30-Year Veteran’s Complete Annuity Sales Presentation

By David Duford - January 03, 2023 - 5 Mins Read

Have you ever wanted to learn more about selling annuities?

In this article, I speak with Scott Bradley, a top annuities sales agent, on how he sells annuities to his insurance leads.

Here’s what you’ll discover in my interview with Scott:

-

- How an annuity sales presentation sounds from beginning to end

-

- How to build rapport and trust

-

- How to position your service as the superior choice to protect against the swings of the market, and

-

- How to get into a annuity sales presentation from another lead source like final expense, Medicare Advantage, Medicare Supplement, or Mortgage Protection.

Let’s begin reading the transcript of the interview below!

NOTE: This is a second presentation after completing another sales presentation for another product.

Scott Bradley completed a needs analysis regarding the client’s existing assets, and asked for a second appointment to share ideas on asset protection with him.

If you want a copy of our needs analysis we give to our annuity sales agents, please contact me here and I’ll email it to you.

Quick Navigation Article Links

The Entire Annuity Sales Presentation Script

David Duford (DD): I am going to be the final expense prospect who is revisiting with Scott. Scott of course is going to be the annuity agent. So let’s get started, Scott.

Scott Bradley (SB): Hey Dave, thanks for having me back today. I really do appreciate it. Last time we chatted you took the final expense policy, which by the way came in the mail. I brought it with me.

But that’s not the main reason for my visit. I wanted to discuss some items that we talked about previously when you mentioned assets and what you wanted to do with your assets.

I specifically wanted to talk about what’s available in the marketplace today.

First and foremost, I see that Mrs. Duford is not with us today. Do you have any problems discussing your finances without her around? Or does she take a big part in deciding your day-to-day finances?

DD: No, I make all the decisions when it comes to financial stuff.

SB: You make all the decisions, okay.

What I wanted to really talk with you about are the concerns you had mentioned about your assets.

What I’m going to do on paper here is write down your assets. How much do you think you currently have in savings and/or investments?

DD: I have $250,000 approximately with a broker.

SB: How long have you been with that broker, Dave?

DD: Years, a number of years, probably at least 10 or so.

SB: Okay. Does he go over specifically with you what you have and where it’s working and how it’s working?

DD: No, not really. I haven’t heard from him in a long time.

SB: Oh, okay. So how did you come across this broker in the first place?

DD: I replied to a direct mail campaign that came in the mail. I talked with them and just decided he seemed like a decent guy.

SB: Okay, so you had no other contact with him other than a piece of mail that came.

DD: Correct.

SB: Does he ever discuss the different types of investments he puts you in or how do you choose your investments?

DD: I don’t know. I told him I don’t want to really lose money, right? I’m at a point in my life where conservation is more important than making more money if that makes any sense, Scott.

So I asked him to just make sure that I’m not losing a lot of money if the stock market goes haywire.

SB: Okay, so you really get upset when you get your statement and it’s kind of a lot less than what you originally had in it, right?

DD: Oh, yeah. I mean this is what I have to live the rest of my life on, so it has to last. I have to keep as much as possible.

SB: Dave, if you’d do me a favor since we’re chatting about this, do you know where your last statement happens to be? Could you get it for me?

DD: Sure.

SB: Ok, so this is off script for a moment: You get your statement out and we’ve got it in front of us. We’re taking a look at it and I’m not making any judgments whatsoever or talking about the statement.

I’m not discussing the individual investments. I’m only talking about the fact that he does have a broker, his balance in that account is right at $250,000, and it looks like it’s non-qualified money, which means that it’s not IRAs or anything else.

And so David, when you get this, and I assume that you get these statements on a monthly basis, how does it make you feel when you see the balance go up and you see the balance go down?

DD: Well, I would normally say I love it when the balance goes up, and of course anybody does, but certainly it’s the down swings that are problematic and concerning, especially as of late.

I don’t feel good about seeing such drops in what I’ve worked so hard to save for.

SB: Have you ever considered making changes when you see those drops?

DD: How do you mean when you say changes?

SB: I mean have you called a broker and talked to him and said hey, what’s going on, why is my account dropping, etc? What’s been his response?

DD: No, and the last time we did this was 10 years ago during The Great Recession, and his comment then was basically the same.

“Just sit tight, don’t worry about these upswings. This is just what happens. It’s part of being in the market.”

So I kind of take that as the same mentality here too.

SB: Wow, that seems to be a cavalier attitude when it’s your money not his money. Would you agree?

DD: Yeah, sure, sure. Easier said than done.

SB: Yeah, that’s what I’m trying to get at. Did he ever mention to you something called a paper loss?

DD: No, what does that mean?

SB: Okay. Well, a lot of brokers often say when your statement goes down in value to not worry about it, it’s just a paper loss.

If they ever say that to you, do they also say to you if your statement goes up in value, don’t worry about it, it’s only a paper gain? The point I’m getting at is we’re talking about real money and we’re talking about real assets.

David, moving forward from that, do you have any IRAs or any type of investments similar to that?

DD: I have $150,000 with the same broker.

SB: Okay. Did he send you a separate statement on those accounts as well?

DD: Yes, here they are.

SB: Okay, so we’ve got two statements here for roughly $250,000 and I see that you have this one invested in the marketplace as well.

Did they talk to you about safety and security and not losing any of your assets when you had them invested? I mean what was his standpoint on that?

DD: Kind of the same conversations as before. I expressed my concerns, and that I wanted to lose as little money as possible, but I didn’t want it to just sit in an account either and not get any interest.

So I asked him to just do whatever you’d need to do to make it conservative as possible if that makes sense.

SB: Okay. I see here, there is something that they’ve taken out of your account with fees. Did you know that you had fees being taken out of your account?

DD: I figured there would be fees, sometimes.

SB: This is roughly $2500 a year on one of your investments. That’s a fairly hefty amount to pay in fees. That’s over $200 a month. How does that make you feel?

DD: Well, since I haven’t heard from him in a while, not too great.

SB: Okay. So what you’re telling me is you want safety and security, and you are not too happy about the fees that you’re paying for the kind of service that you’re getting.

Let me finish asking a couple of questions and then I’ll share with you some options. I assume that you’re retired now, aren’t you?

DD: Correct, yes.

SB: Okay, and what type of income are you bringing in from retirement right now?

DD: I draw $2000 from Social Security. My wife draws $1300.

SB: All right. Do you have any investment properties?

DD: Yeah, two. They’re free and clear. They cash flow $1000 a month each.

SB: Okay, so to recap here, you’ve got roughly $2000 a month coming in from your properties. You have $2000 a month coming in from social security, and your wife brings in $1300 a month.

That gives you roughly $5300 a month in income. Right?

DD: Right.

SB: Now, my question to you is this – what type of expenses do you have going out monthly? I mean how much do you spend?

DD: We spend a big chunk of that, but we save a little bit, maybe about 10-15%, nothing abnormal. Just regular expenses any normal person would have, with travel here and there.

SB: Okay. Now I know you have the life insurance that we wrote with you last time, that $25,000 policy, but do you have any other life insurance in effect right now?

DD: No.

SB: Okay. So in the event of your passing, how are you planning to continue to make sure that your wife has enough income to continue your lifestyle that you have now?

DD: I figured we’ll keep the investment homes, they’ll go to her, and then I’m assuming she gets my Social Security and then whatever assets I have in my IRAs and with my broker. Hopefully, that will be enough to take care of things.

SB: Yeah, the rule on Social Security is basically the spouse making the greater amount is the amount that sticks around. For example, if you pass away, your $2000 will now become the income for her, and her $1300 goes away. So that will reduce your income basically from $5300 to around $4000 per month.

Now, you say that you’ve got those two properties that you have, and you told me they were worth roughly half a million dollars.

In talking about those properties, have you found it fairly easy to keep renters in the properties?

DD: No more difficult I think than the average. You get a renter in, they stay a couple of years, and it goes vacant, got to do some fixing up, and then get another renter in. So just what I would expect from most rentals.

SB: Okay. Have both of them been vacant at the same time before?

DD: Yeah, maybe for a month or two at the most, yeah.

SB: Okay. So what I’m seeing is that the income from the properties can vary quite a bit. And if they get behind or if you have to do repairs or you have to do anything to the homes, you see that there’s some fluctuation that comes with that income.

DD: Sure.

SB: I’m going to ask you a very, very crazy question right now, all right? And you’re going to laugh when I ask you the question.

If you had:

A) the opportunity to a greater rate of return but you could lose all of your money

B) you can have less of a rate of return, but you could lose some of your money , or

C) you could have a smaller rate of return but you could lose none of your money at all…

Which of those options would you go with?

DD: At this stage, option C. I’m more concerned about conservation of what I’ve accumulated, instead of taking a chance.

SB: Okay. Now you just finished telling me that you wanted conservation of your funds, you didn’t want to take a chance with your money.

Yet, I’m looking at the statement that you showed me, the $250,000 as well as the $150,000, and they’re invested in items that go up and down with the market.

Now, I’m sure that you’ve seen the market in the past few months, and all that has happened since COVID-19. How does that make you feel, Dave?

DD: Like I said, not comfortable. I don’t like it at all. I don’t know what to expect. Some days it’s up, great, some days, it’s down, horrible.

SB: All right. Well, there are some things that I can share with you that I believe will maybe give you some answers.

First I need to give this disclosure: Number one, I’m not a securities advisor. I used to be a long time, but I’m not anymore.

I can’t tell you whether to buy or sell any specific security. I can’t tell you whether it’s a good deal or whether it’s a bad deal, because I’m not licensed to do so.

However, I can share with you this much:

What we’re going to talk about today has zero risk. And what I’m specifically going to talk to you about are items that grow in value if the market happens to be on an upturn, and yet if it goes on a downturn, then specifically, they stay flat.

In other words, does not gain, does not lose where the rest of the market takes a loss.

So you get advantages with participating in the upside of the market, but you don’t have any of the disadvantages of the downside of the marketplace.

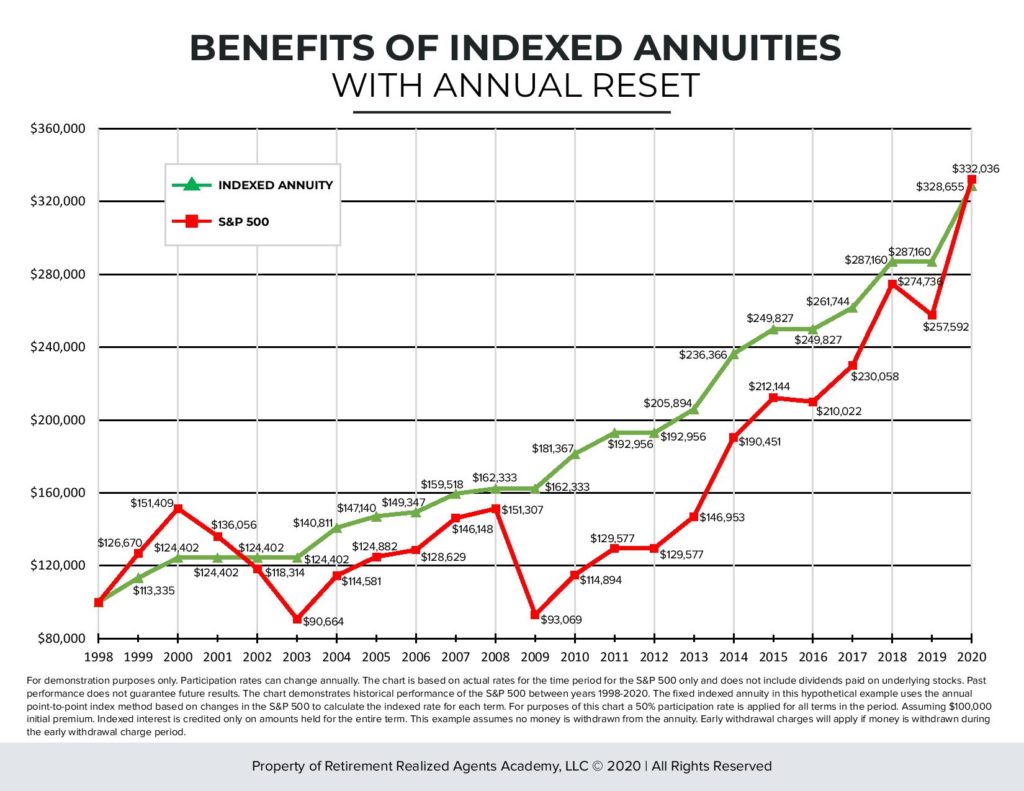

Now, there is a chart that I’m going to share with you. It charts the rise and fall of the market and where your money would be at if the market rose or fell.

As you can see, when the market does well, your annuity investment increases, as does the type of investment you currently have.

But when the market falls, a regular investment like you have now also falls. But the annuity investment stays the same.

So my question to you is, David, seeing how your money can grow and grow safely. How does that make you feel?

DD: Well, I like that because I can think back to specifically 2008-2009. The feeling of a 30% to 40% drop is just a horrible feeling. Right?

And your broker is telling you just be patient, the pain will go away eventually. Obviously, it didn’t for a number of years.

It would’ve been a lot nicer to not lose anything, especially at this point in my life. To know that at least what I’ve accumulated is safe, even if things go bad, even a 0% return seems pretty appealing in this day and age.

SB: Okay. What I basically described to you is what an annuity is, and let me break it down even further.

Most people understand what a CD is, a certificate of deposit with a bank. Our certificate of deposit with a bank has an amount of principal. It has a set determined interest rate. It has a specific period of time, and it has penalties if you pull the money out ahead of time. Okay? Are you familiar with that?

DD: Yeah, sure.

SB: Okay. The other thing that I’m going to mention to you is an annuity. An annuity has some of the same concepts that a certificate of deposit does, but the main difference is it’s not backed by a bank, it’s backed by the full faith of an insurance company.

Let me explain to you specifically the differences between insurance companies and banks. Banks operate on a system of what’s called debt or fractional reserve.

That means the way a bank makes money is it loans out money to folks and it gets interest for the amount it loaned out.

In order for a bank to operate, they have to be a member of the FDIC. FDIC is the Federal Deposit Insurance Corporation. It is not the federal government, it is an insurance corporation.

And what they are doing is they are insuring the deposits up to a certain amount in the bank to give people a sense of security.

It was actually created in 1932 in the middle of the Depression to make folks feel happier about putting their deposits into banks.

Now, insurance companies operate not on debt, but they operate on a cash basis. In other words, if an insurance company loans money out to somebody, they’re operating from cash reserves not cash debt.

There is a big difference here because when you have debt, you have risk. When you have debt, you have the chance of people forfeiting or not paying their debt, and you’ve actually lost out on that money.

So in the entire history of insurance companies, there has never been a single insurance company that has defaulted on any single insurance policy that they have placed at any period of time.

Banks can’t say that. Banks have risk. As far back as 2008, many many very large banks failed due to the crisis with lending in the mortgage industry.

This didn’t happen with insurance companies. They didn’t lose any money and they didn’t lose any of their value.

Now, I’m talking about a standard insurance, I’m not talking about variable insurance which is linked to the stock market, I’m talking about standard insurance.

So that’s the difference between a CD which is with a bank and an annuity which is with an insurance company?

The CD with a bank is backed by debt instruments and this annuity is backed by the full faith and power of the insurance company, and cash, because insurance companies have to have one-to-one cash versus a bank.

A bank can loan out up to 100 times more than what they’ve got in deposits. In other words, they don’t have to keep much at all in reserves.

Banks have to keep 10% in reserves, insurance companies have to keep 100% in reserves.

So safety and security is one of the key fashions that you’ll get with an annuity. An annuity also has some fashions that CDs don’t have.

First of all, they grow tax-deferred. And what that means to you is you don’t have to pay any tax whatsoever on any of the gains that you have within the annuity. With a CD, they’re taxable, you have to pay taxes on it.

The investments that you have with your broker are taxable. In other words, at the end of every year, if you have a gain in your account you have to pay taxes on that gain.

With an annuity, they grow tax-deferred. And what that means is as long as you’re not taking the money out, it grows and grows and grows and you don’t have to pay taxes on that money until you take it out.

Now, once you start to take it out, yes you do have to pay taxes. The last amount that went into the account is the first amount that’s going to come out of the account.

So the first thing that you’re going to do is you’re going to take gains on the account, and you’ll have to pay taxes on those gains that you have while in the fixed annuity.

However, going back to the chart that we talked about earlier, if there has been significant gains in the market, the fixed annuity is going up as well.

For example, if we take 2008-2009, and we go to where it says $162,232 on the fixed indexed annuity and we go one year further, it still has $162,333.

You might say, “Wait a minute, that’s not a good deal, there was no gain whatsoever on my money.” But let’s compare that specifically to the S&P 500.

At the end of 2008 it was $151,307. Look what it did in one year. It went all the way down to $93,067.

Now, that is approximately a 40- 45% loss in your assets, whereas on the fixed indexed annuity it started out at $162,333, and a year later it was still $162,333.

Who do you think is going to be the happier investor? The one that’s in the marketplace or the one that’s in the fixed indexed annuity?

DD: Right, I agree.

SB: Now, that being said, would you like to protect your money from any downturns that have been in the marketplace?

DD: Sure. Of course.

SB: Okay? There’s a saying that we have, it’s called “zero is my hero.” And I’d like to give you a short quick story of what happened to me specifically.

As you know, the marketplace and the S&P 500 went up like crazy some years ago. Back in 2007, I had a client who had a program similar to this, and she had gained 14%.

I was reviewing her statement, and the whole time she wasn’t happy at all. And I thought to myself, “Wow, we had a 14% return and she’s not happy, what is it going to take to make this individual happy?”

So I left the money alone, came back at the beginning of 2009 and said, “Gosh, I’ve got zero return here, and if she wasn’t happy with 14%, how is she going to respond when she gets 0%?”

Well, this lady was so excited and so happy that she gave me big ol’ hug and said, “Yeah, I didn’t gain anything, but I didn’t take a 30% something loss like my neighbor did. I am so happy, it’s just amazing.”

That is the power of a fixed indexed annuity.

Now, we’ve discussed a lot of things today and we’ve gone over a lot of items.

And from what I’m hearing from you, number one concern is you don’t want to take any losses on your funds. Is that what I’m hearing from you?

DD: Right.

SB: Okay. You want to make certain that in the event you pass away, you want to take care of your wife and make sure that she has enough income to live on, is that right?

DD: Correct.

SB: Okay. Currently, because of your Social Security and because of the income that you have coming in from your houses, you’re not in a specific need for income right now, is that what I hear you saying?

DD: Right, correct.

SB: Okay. So it kind of make sense to move your assets in a safe and secure way that will take advantage of the marketplace yet at the same time protect what you currently have.

Am I putting the pieces of the puzzle together correct here?

DD: Yes.

SB: All right. Now, one of the things by law I am required to give you is the buyer’s guide to annuities, that is created by the National Association of Insurance Commissioners.

It’s a 20 page guidebook written to give you answers to specific questions. I have to give this to you whether you choose to do business with me or not.

The second thing I have to give you is what we call an illustration. Now, we’ve talked about a lot of different items and what I want to do is give you an illustration that shows specifically that you’re taking income or not taking income from the amounts that you have.

The thing that I do differently than most insurance agents is that I don’t come across and illustrate to you a 10, 12, 14, 16% rate of return.

I’m going to show you an illustration that has zero rate of return, meaning your money does not gain, and your money does not lose whatsoever.

SB: Then on the next page, I’m going to go back and I’m going to show you a very conservative 4% rate of return. And what that means is over time your money will gain at 4%.

Typically, what we’re trying to do in a safe, secure environment is make certain that your money can grow and at the same time get between a 2% to 6% gain on your money.

So that being said, here is your illustration, here is your buyer’s guide to annuities, and here is the company brochure with more information.

Would you like to protect your assets that you currently have?

DD: Sure, sounds good.

SB: Okay, off script here: At this point, I start taking information to write down on an application.

Questions About The Annuity Sales Script

DD: How much would you have written up in this example?

SB: Well, first and foremost, you’re very unique. I would not write more than half of what they have in an annuity, because an annuity does tie up money for a period of time.

And specifically, I didn’t talk about surrender charges, I didn’t talk about time, I didn’t talk about everything involved. I would go over that in a specific annuity that I’m going to recommend to a prospect.

I would show them an illustration with the surrender charge. And during this time frame, I would take $170,000 of the non-qualified assets and move them over.

I would probably take $100,000 of the IRA. I would not take all of their assets because you really don’t want to put a person in a fix that they can’t get access to their assets.

It’s very crucial you explain surrender charges, and very crucial you explain the period of time that you’re talking about. This is not a short-term basis.

How To Handle The Broker

Also, we talked very much in depth about what the broker is going to say to them in the event that they want to make changes.

They will say, “Well, that’s going to cost you all kinds of fees.” Well, actually, there are no fees with this unless we take the income rider which allows your money to grow in separate accounts and would be less than 1% in fees. I would show that to them on the illustration.

The broker might also say, “You’ve been with me for 10 years, have I not done you good?”

Well, when the marketplace was changing or the marketplace was on a downturn, did you give me a call and explain the differences to me? Did you tell me about this? And usually the answer is no.

There was a very large brokerage house that sent out a memorandum to all of their agents specifically telling them to focus on their accounts that are half a million dollar and higher.

They said to get to the ones below half a million dollars when you can but don’t worry about them, you want to call your A clients first.

So going back to our roleplaying with Mr. Duford, because you have less than a half million dollars, do you think your broker is going to call you?

How many calls have you gotten in the past 10 years telling you to reallocate your assets.

And from what I’m hearing Mr. Duford says he’s not had any contact with this guy in the past 10 years. So even though there is a loyalty there that they don’t want to leave, they need to know that brokers are making money on you whether your account goes up or whether your account goes down.

On the other hand, with fixed indexed annuities, it doesn’t matter if the market goes up, it doesn’t matter if the market goes down, it doesn’t matter if the market stays the same, your money is protected 100% and you’re not going to take any losses or pay any fees to have somebody manage your accounts.

And by the way, talking about managing accounts, is there anybody that really manages accounts? No, they don’t. A computer manages the accounts.

Computers shift money all the time. And every time they shift money around, depending on how the account is set up, that broker is going to make a fee from selling a new product.

The Benefits Of An Annuity

So what I want to explain to everybody is the safety and security of an insurance company versus a bank versus a stock brokerage house versus the marketplace.

I show them how no one has ever taken a loss in an annuity, and they can’t say that about banks. You can’t say that about stock brokers and you can’t say that about any kind of mutual fund account.

I show them that number one, once you want an income, you can create an income depending on the time frame of the annuity.

And you can turn your income off too. It is so flexible that people love it when they understand what an annuity can do for them.

Tax deferral, that’s a big big deal, because if you can pay your tax deferral versus taxable growth, it is a much better deal.

Remember, you need to give the prospect a buyer’s guide to annuity, you have the company brochures, and you have the illustration that you create.

It’s really important that insurance agents give the client those things. If they don’t, there could be consequences.

Number one, someone like me is going to walk in behind you and ask a specific question: Did you got those items? And if you didn’t, I’m going to look at you and say, “Oh wow, by law, they have to give this to you because we’re talking about annuities.”

And what does that do? That is going to create a question as to your integrity, as to why you didn’t give me those things to begin with.

Taking An Income With An Annuity

I also leave the income section alone. Meaning I don’t start taking income for five years. After 5 years have passed we can start talking about income and your prospect will see specifically that they’re going to get income like crazy for the rest of their life.

They really like that. But I leave it alone for five years regardless of what the market has done.

I am not giving them a proposal based on what the market has done in the last 10-20 years. I’m just not going to do it, because I don’t know what the market is going to do.

Gold And Silver Questions

I also get the question, “How do you feel about investing in metals such as gold and silver?”

My answer is, “Do you know what the price of gold is going to do tomorrow? No? Okay. Do you know what it’s going to do in a year? No.”

I like to deal in safe money, meaning I like to deal in specifics and deal with what I understand and can show to people. As you can see with this illustration, I’m showing 0% growth, 0. But what that also shows is protection of your money.

Are there times where the S&P 500 will outgrow a fixed indexed annuity? Sure. There are times that is going to happen. But the majority of the time, your money will do better in a fixed annuity because it doesn’t fall with the market.

If I’m getting nods from the individual the entire time I am doing my presentation, I’ll start to write an application.

I do a paper application, an e-app. The reason for that is because the paper application takes it page by page and you fill out block by block, and the customer is more comfortable with that type of situation.

That’s an annuity presentation pretty much from soup to nuts.

Annuity Objection Handling

DD: What are the top three objections you’ll get, Scott? And how do you overcome them?

1. How safe are annuities?

SB: Well, first of all is safety. What kind of assurance do I have with the safety?

And I explain to them about insurance companies and I go over again, the cash backed company versus fractional type reserve companies. I explain to them how that works.

I also explain to them that we don’t have something called margin. We don’t have things that are speculative in the marketplace.

2. How long do I have to have an annuity?

Second objection that I possibly get is the length of time. I ask them a question and say well, how long has your money been with a broker?

Typically you’re going to get 10 to 15 years that they’ve been with a broker.

3. How do I know my money is truly working for me and is safe?

The third thing is how do I know that my money would be working for me? How do I know that it’s not going into the marketplace?

Well, number one, your money would not be going into the marketplace, because this is a fixed indexed annuity.

We’re using the S&P 500 as a reference only and we’re only using that as an index to go by. We’re not investing your money in the marketplace at all.

I tell a lot of prospects where I personally have my funds invested. My personal retirement income is with a fixed indexed annuity.

Now, me understanding the marketplace as much as I do, I could go with any investment whatsoever.

But I choose to go with safety and security because I am 60 years old and I do need to have safety and security at this time in my life. I just tell people to try it out.

What other questions do you have, Dave?

Summary

DD: Well, the idea of handling the objections would be a big one. How you present the presentation obviously. It’s not just about gains, it’s certainly about security and safety.

You weren’t pushing a bunch of numbers around. I imagine somebody who is a basic blue-collar person with a little money to go after would probably get this without much confusion.

And I think the perception is that annuities is difficult and hard. There are a lot of moving parts and certainly, there is, but you’ve taken the complex and made it simple in my estimation.

SB: And that’s the whole thing. You’ve got to remember, these people are not registered investment advisors that you’re talking to, they’re people that may have had a pool installation company or a roofing company and they were good at saving money.

And that’s all you’re doing is helping the individual protect their hard earned assets, period, end of story.

And when that happens, they seem to be happier or more comfortable, they don’t want to take risk at this age.

When we started talking I believe you said you were 67 years old. And at 67 years old, that is way too old to start taking risk. Imagine, at 67, if the marketplace did what it did in 2008.

And it takes all the way til 2013-2014 for it to correct itself, six years or so. That puts you at 73 years old. Can you afford that kind of timeframe? And that’s what we’re talking about.

DD: Yeah, I agree. I think that’s what agents should really be focusing on is risk and preservation. I think that’s their critical discussion point.

Any last thoughts you want to throw in there, Scott, before we wrap it up?

SB: When we deal with final expense, we’re typically dealing with people that don’t have money assets. However, there are a lot of people that are very secretive about what they have.

Often they do have assets. Just because they buy a $15,000 or $25,000 policy from you, does not mean that they don’t have close to half a million dollars sitting in some type of investment somewhere.

Grandma has a lot of money put aside sometimes. And she didn’t want you to know abou it. That’s often what we find.

So I ask the questions and then I say when you get your statement from the different companies, how does it make you feel when it goes down? And that’s the key. It’s an emotional sell, it’s not a logical sell. And that’s what it boils down to.

DD: I think that summarizes a lot of people’s questions on how this stuff is presented in a simplified manner. So Scott, thank you for time and appreciate you today.

SB: Sure. Thanks David.

Interested In Selling Annuities With Scott And David?

To learn more about contracting with my national agency, reach out here.

We have access to all sorts of benefits for final expense agents, including:

-

- Top contracts with the best annuity carriers. David Duford recruits and operates at FMO/IMO levels, giving him buying power to offer commission levels to agents and agencies others cannot match.

-

- Affordably-priced, high-quality lead programs for direct mail, Facebook, and telemarketing leads. David does not profit from the sale of leads, only referring you to sources with a track record of success.

-

- An endless supply of top-notch prospecting and sales training at your fingertips.

-

- Weekly sales training calls with David, ride-along training opportunities with David and his team, and direct phone/text access to David and his annuity team when you have case placement and sales questions (yes, David answers his own phone =).

-

- Additional training and support for agents interested in cross-selling Medicare Advantage, final expense, or growing their own insurance agency.

-

- Check out David’s Agent Success Stories here for more insight.

Reach out to David by starting here. Talk soon!

January 03, 2023

January 03, 2023

January 03, 2023